Here’s how to understand the basics of – and prepare your – own cash flow statement, as well as some ways to extract juicy insights from your statement. The cash flow statement is the ultimate source of authority on your business’s accumulation and use of cash. Regardless of the method, cost accounting standards for government contracts the cash flows from the operating section will give the same result. The left-hand side records various sources of cash inflows and the right-hand side records the use or outflows of cash. Cash flow from operations are calculated using either the direct or indirect method.

How to track cash flow using the indirect method

Note the section of the statementof cash flow, if applicable, and if the transaction represents acash source, cash use, or noncash transaction. LO 16.6Use the following excerpts from VictroliaCompany’s financial information to prepare a statement of cashflows (direct method) for the year 2018. LO 16.3Note payments reduce cash and are relatedto long-term debt. Do these facts automatically lead to theirinclusion as elements of the financing section of the statement ofcash flows?

The indirect method of calculating cash flow

These include our video training, visual tutorial, flashcards, cheat sheet, quick test, quick test with coaching, business forms, and more. LO 16.5If you had $100,000 available forinvesting, which of these companies would you choose to investwith? Support your answer with analysis of free cash flow, based onthe data provided, and include in your decision whatever otherreasoning you chose to utilize. LO 16.4Provide the missing piece of informationfor the following statement of cash flows puzzle. A positive effect could also be thought of as a source of cash, an increase in cash, or a positive amount on the cash flow statement. Cash flow is the total amount of cash that is flowing in and out of the company.

Does not Replace the Income Statement

Greg purchased $5,000 of equipment during this accounting period, so he spent $5,000 of cash on investing activities. Purchase of Equipment is recorded as a new $5,000 asset on our income statement. It’s an asset, not cash—so, with ($5,000) on the cash flow statement, we deduct $5,000 from cash on hand. These three activities sections of the statement of cash flows designate the different ways cash can enter and leave your business.

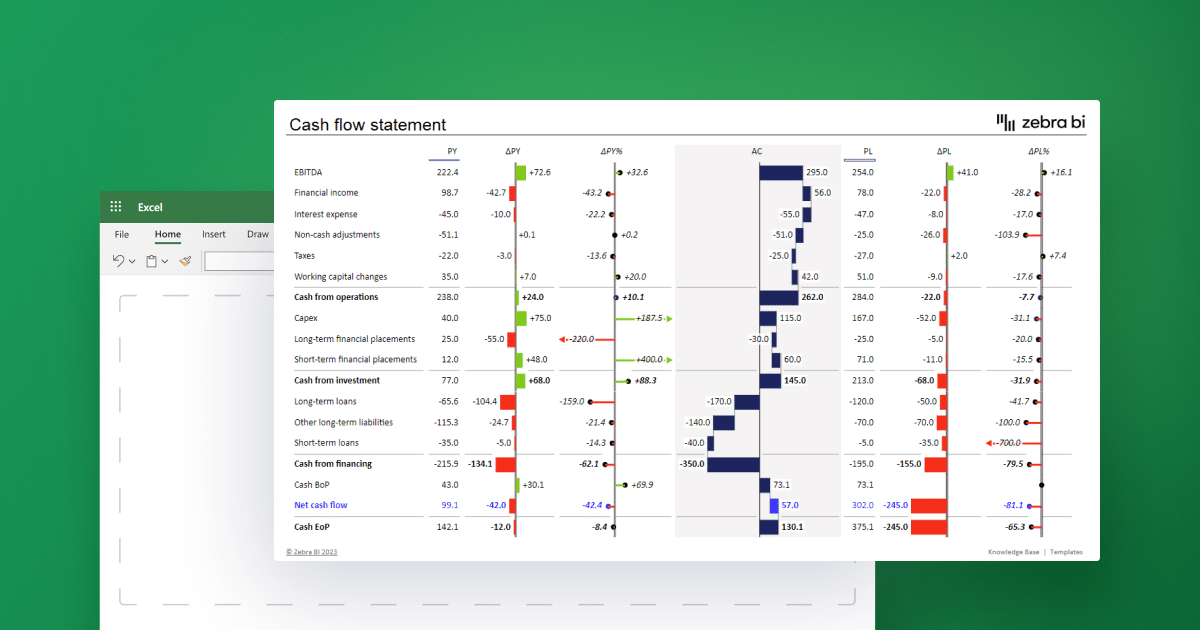

LO 16.3Use the following information from CoconutCompany’s financial statements to prepare the operating activitiessection of the statement of cash flows (indirect method) for theyear 2018. LO 16.3Use the following information from BerlinCompany’s financial statements to prepare the operating activitiessection of the statement of cash flows (indirect method) for theyear 2018. Financing activities within the cash flow statement provide insight into how a company funds its operations and growth. By analyzing cash inflows and outflows related to debt, equity, and dividends, analysts can assess the company’s financing strategy.

Increase in Accounts Receivable is recorded as a $20,000 growth in accounts receivable on the income statement. That’s money we’ve charged clients—but we haven’t actually been paid yet. Even though the money we’ve charged is an asset, it isn’t cold hard cash. Using the direct method, you keep a record of cash as it enters and leaves your business, then use that information at the end of the month to prepare a statement of cash flow. While income statements are excellent for showing you how much money you’ve spent and earned, they don’t necessarily tell you how much cash you have on hand for a specific period of time. A cash flow statement is a regular financial statement telling you how much cash you have on hand for a specific period.

Revenues and expenses are not separately reported on the cash flow statement (unless they are not paid or received in cash). However, if you haven’t paid the interest, it appears as a current liability on your balance sheet. The unpaid interest amount is added under adjustments in working capital in the operating activities section of the cash flow statement. Note that interest payments on debt don’t appear under this section.

But cash isn’t literally leaving your bank account every month. Cash flow statements are also required by certain financial reporting standards. Investing and Financing sections are the same for the direct and the indirect method.

- Clearly, the exact starting point for the reconciliation will determine the exact adjustments made to get down to an operating cash flow number.

- The financing activities, they deal with our investors and our creditors, and it’s the rest of our balance sheet.

- Similarly, if the balance of accounts payable increases by $5,000, add it to the cash flow from operating activities.

- LO 16.6Use the following excerpts from FromeraCompany’s financial information to prepare the operating section ofthe statement of cash flows (direct method) for the year 2018.

- We begin with reasons why the statement of cash flows (SCF, cash flow statement) is a required financial statement.

Cash transactions impacting stockholders are reported as a financing activity. However, it does not measure the efficiency of the business in comparison to a similar industry. This is because terms of sales and purchases may differ from company to company. Management can use the information in the statement to decide when to invest or pay off debts because it shows how much cash is available at any given time. Cash-out transactions in CFF happen when dividends are paid, while cash-in transactions occur when the capital is raised. Transactions in CFF typically involve debt, equity, dividends, and stock repurchases.

If you’re not a young company and you see a negative cash flow from operations, you have a reason to worry, even if the cumulative net cash flow is positive. Expenses recognized but not paid, such as deferred income tax expense, must be added back into the net income figure. Deferred expenses are available on the asset side of your balance sheet. Remember that the indirect method begins with a measure of profit, and some companies may have discretion regarding which profit metric to use.

The term cash flow generally refers to a company’s ability to collect and maintain adequate amounts of cash to pay its upcoming bills. In other words, a company with good cash flow can collect enough cash to pay for its operations and fund its debt service without making late payments. LO 16.6Use the following excerpts from SwahiliaCompany’s financial information to prepare a statement of cashflows (direct method) for the year 2018. LO 16.3Analysis of Longmind Company’s accountsrevealed the following activity for Equipment, with descriptionsadded for clarity of analysis. How would these two transactions bereported for cash flow purposes?